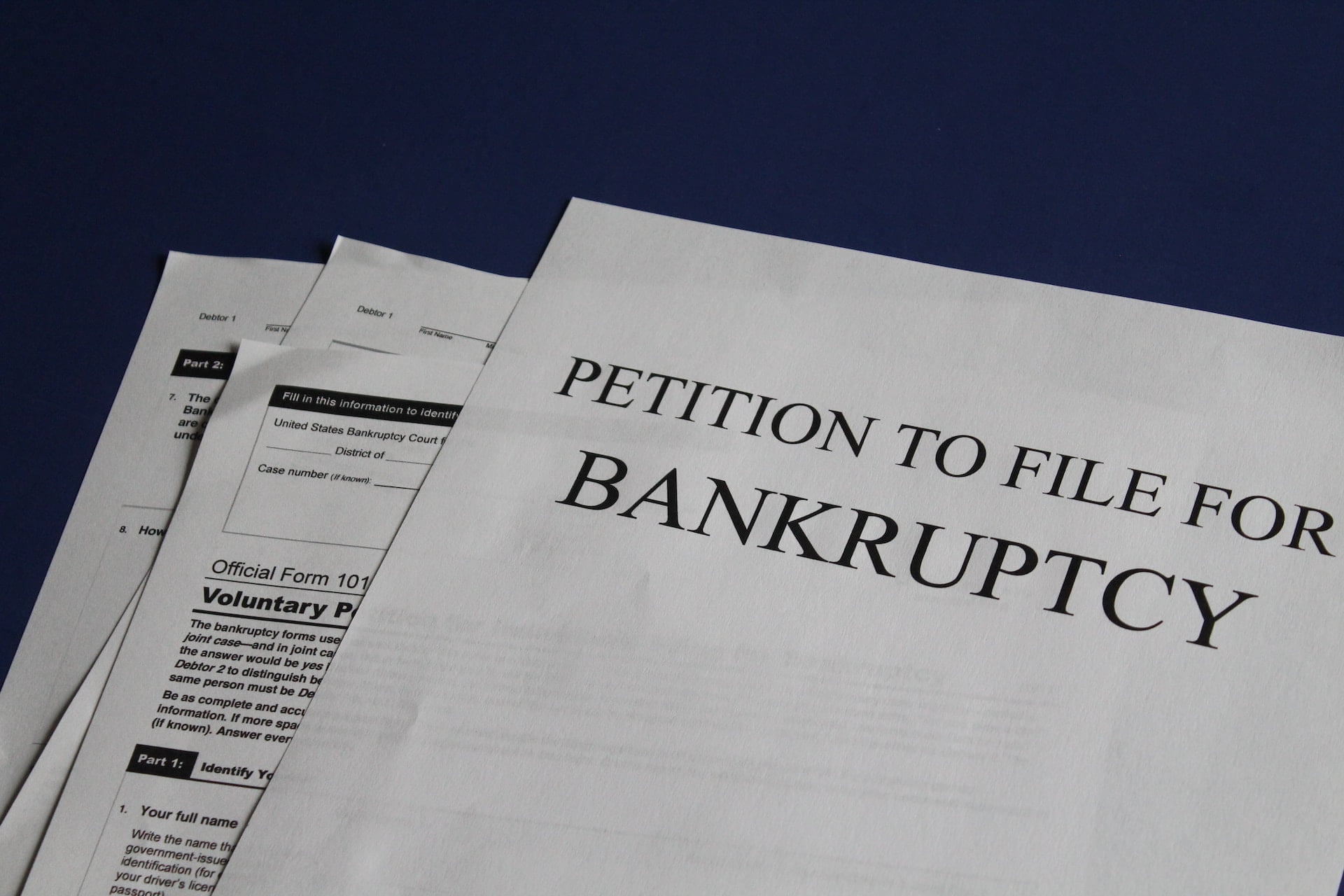

Las Vegas-based cryptocurrency custodian, Prime Trust, has taken the step of filing for Chapter 11 bankruptcy protection on Monday. This move marks another setback for the fintech company during what has been referred to as a prolonged “crypto winter.”

On August 15th, in its filing, Prime Trust revealed 25,000 to 50,000 creditors and liabilities ranging from $100 million to $500 million. Its assets, including Prime Core Technologies Inc., Prime Trust LLC, Prime IRA LLC, and Prime Digital LLC, are valued at $50 million to $100 million.

According to a related press release, Prime Trust plans to submit motions to the Bankruptcy Court to evaluate strategic choices. These options encompass potential asset sales and ongoing operations. Notably, recent problems involving Nevada Regulators and Creditors could complicate the quest for a suitable buyer.

Prioritizing transparency and clients, Prime Trust taps ex-Bank of Nevada president John Guedry for Chapter 11 restructuring. Judge Susan Johnson will oversee this process, while the firm will function as “debtors-in-possession” under the court’s direction.

Factors Behind Prime Trust’s Bankruptcy Filing

The trigger for Prime Trust’s bankruptcy filing was a cease-and-desist order issued by Nevada’s business regulator on June 21. This order followed the regulators’ move to shut down the cryptocurrency custodian due to its precarious financial situation.

According to reports, the firm had amassed significant debts in both fiat and cryptocurrencies. Its liabilities consisted of more than $85 million in fiat and $69.5 million in cryptocurrencies. Surprisingly, Prime Trust had access to just $2.9 million in fiat and a slightly larger sum of $68.6 million in cryptocurrencies.

The order highlighted Prime Trust’s dire financial condition, impacting its capacity to fulfill customer withdrawal requests. Consequently, Nevada regulators acted decisively, placing the company into receivership by late June. This move effectively suspended Prime Trust’s operations, rendering it incapable of catering to its customer base.

This development came after a string of challenges encountered by Prime Trust and its affiliated firms throughout the previous year. Prime Trust’s subsidiary Bank filed for bankruptcy, alleging mismanagement by former CEO Scott Purcell.

Furthermore, Prime Trust’s partner, Abra, encountered legal issues, as it received a cease-and-desist order in Texas over allegations of securities fraud.

Prime Trust Regulatory Challenges and Custodial Crisis: A Deepening Predicament

These regulatory setbacks, along with Nevada’s cease-and-desist directive, led to the suspension of customer withdrawals. In response, Many cryptocurrency firms with funds at Prime Trust promptly reassured clients and initiated asset withdrawals. However, companies like Coinbits found their customer funds trapped within the bankrupt custodian.

The situation escalated when the Nevada Financial Institutions Division (NFID) stepped in to shutter Prime Trust. The division disclosed its vigilant oversight of Prime Trust’s financial stability, while exploring avenues like acquisitions or mergers.

However, the division voiced apprehensions regarding Prime Trust’s breach of fiduciary duties to its clients, which constituted a violation of Nevada’s trust laws.

Reports reveal that Prime Trust’s mishandling of customer funds for withdrawals commenced in December 2021. This misstep occurred after the company lost access to certain customer cryptocurrency wallets.

The actions taken by the NFID shed light on the larger difficulties confronting Prime Trust, casting it as a cautionary example within an industry characterized by both potential and unpredictability.

Read More:

Binance Connect to Shut Down Operations on August 16

New Financial Statement Reveals Donald Trump Possesses $2.8M in Ethereum Wallet